The Group of Seven industrialized nations is 24 days from imposing a cap on the prices at which Russia’s oil refineries are allowed to sell the fuels they make. It’s another historic moment for the global petroleum market.

If all goes to plan, buyers of Russian fuels will only be allowed to tap vital G-7 services including ships and tanker insurance for the cargoes if they pay below as-yet-unspecified price caps. Such measures began for crude oil on Dec. 5, setting an upper threshold of $60 a barrel.

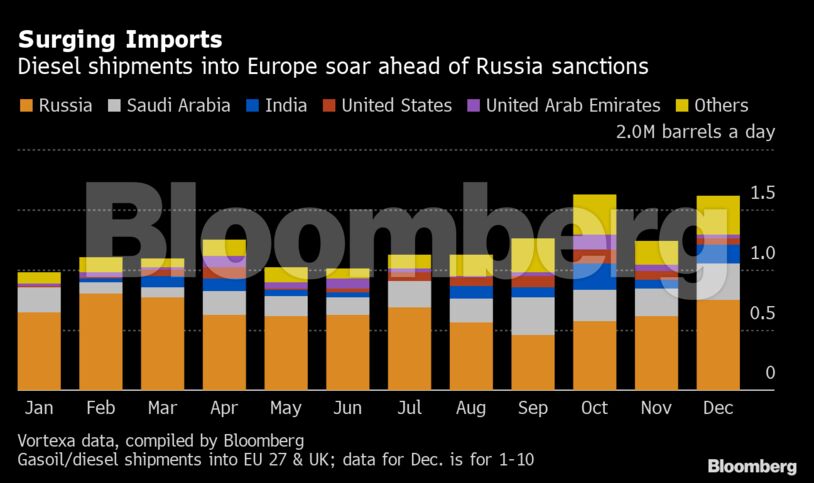

The measures, in tandem with a ban on almost all refined fuel imports to the European Union from Russia, could cause havoc if the thresholds are set wrong for the markets they’re targeting. The move will force some tankers to sail thousands of miles further to get cargoes to buyers.

“We expect that most crude oil exports from Russia will continue to find buyers,” the Energy Information Administration said in a report Tuesday. “But we expect the sanctions on petroleum products will cause greater disruptions to Russia’s oil production and exports because finding alternative buyers as well as transportation and other services to reach those buyers is likely to be more challenging.”

The easy solution would be to set the cap at high enough levels to keep the fuels flowing, as they did with oil. The question is whether there’s the political will for such an approach, when some nations, especially EU member states, want to guarantee Moscow loses revenue.

Here are some of the things the G-7 will have to weigh up:

1. Many Products

The G-7 looks set to introduce two caps: One for those fuels have historically been cheaper than crude, and another, higher threshold for more expensive ones.

That approach has the beauty of simplicity but the markets being targeted are not simple.

There are numerous mainstream oil product categories to deal with, including better known ones like diesel and gasoline. There are others too — fuel oil, naphtha and something called vacuum gasoil — that help to keep global refining and petrochemicals systems functioning efficiently.

Even within those broad groupings, there are numerous subset products, each of which might have different qualities — be it their sulfur content, density or metals content — that make how they trade unique.

Some products hold hidden importance. Vacuum gasoil, for example, is what’s known as a feedstock that many non-Russian refineries process to make other fuels. Naphtha can be used in the production of gasoline or plastics.

So the impact of the caps on individual fuel markets will depend on where the thresholds are set. Diesel is presently trading far above gasoline, for example. If the upper cap is low enough to depress the price of gasoline, then it could be even more dramatic for diesel.

The same would apply to the lower cap. Target high-sulfur fuel oil, which trades well below naphtha, and naphtha could be hit harder. But target naphtha, and the impact on fuel oil would be relatively small.

To add to the complexity, some fuel prices will trade around the same level as crude. How will they be dealt with?

2. Crude Precedent

Since the December cap, Russian crude prices varied significantly based on the location the barrels are exported from. The nation’s flagship Russian grade Urals is trading far below the threshold.

That’s not really down to the cap. It’s because it’s exported from the country’s western ports and requires transportation thousands of miles to a handful of large buyer countries in Asia, particularly China and India.

At the same time, crude from Russia’s eastern terminals is holding well above the cap because it requires so much less transportation. That oil is likely moving outside of the price cap on so-called shadow-fleet tankers.

The lion’s share of the oil products that come out of Russia are from its west, likely facing the same dynamics as Urals. And it will have to go to buyers who often already have plentiful supply of those same fuels from existing suppliers. Some countries will make what they need for themselves and don’t need imports from Russia.

But given that some of the fuels are already discounted to crude, and given Urals is already cheap, and given potentially more complex freight dynamics, the price impact of Europe’s ban and the price cap is unknown.

Could fuel oil price at a level at which Russia’s refineries don’t wish to sell it? If so, it may not take long for some crude processing to be halted.

3. Shipping Complications

Once prices are capped, anything that disrupts access to shipping will affect a market that’s more complicated than crude oil transportation.

Last year, the nation accounted for 9.3% of the world’s seaborne, refined fuel exports while the comparable figure for crude was about 8.8%, according to data from Clarkson Research Services Ltd. compiled by Bloomberg.

When the ban starts, fuel oil — the residue from refining that often gets burned on ships or in power plants outside Russia — will also become subject to the cap. That moves on the same tankers as crude, although Clarkson categorizes it among refined petroleum products.

Oil products have further shipping complications, too. Unlike crude, a tanker that moves one kind of refined fuel can’t always switch to hauling another type straight away without causing cargo contamination. Its internal tanks may well need cleaning.

The trade in such fuels has also long been dominated by smaller vessels that are less suited to the long-distance deliveries that will become more common after Feb. 5.

Vacuum gasoil has a relatively unique status. If it is to move on a ship that previously transported crude, then the inside of that vessel’s tanks must first be cleaned. It could go on a vessel that previously transported, say, gasoline, but then the tanker would have to be re-cleaned before it could move gasoline again.

It will be challenging to run the fleet of refined fuel tankers as efficiently after Feb. 5.

4. Shipping Complication II: Ice

Much of Russia’s oil products exports trade has been carefully calibrated down the years to take relatively small consignments of fuel on relatively small tankers on short-hop voyages to Europe.

It has been organized in a way that recognizes that Russia needs tankers deal with Baltic Sea waters that can ice over in the coldest winter months. Specialist ice-class vessels exist for the trade, but are a relatively small part of the fleet’s overall capacity.

So it’s unlikely these ships can now shuttle thousands of miles further without creating fleet shortages.

“The lack of smaller tankers and different specifications for refined products by different regions may make it more challenging to divert refined products to other markets,” said Giovanni Staunovo, commodity analyst at UBS Group AG. “Also, the main buyers of Russian crude are not short refined products.”

It may depress the prices Russia gets if the cargoes have to get transfered onto other vessels for onward transportation. Higher freight costs have been a key contributor to Russian crude prices falling.

5. Fuel Surge

The greatest risk of all, ultimately, is the combination of a lost European export market and caps that are set at levels that prevent Russian supply moving to other regions.

An undesirable scenario for G-7 officials — especially the White House, which has emphasized risks to prices throughout this process — would be that there is a significant net loss of fuel supply.

Prices, especially in Europe, would most likely jump.

6. Arbitrages

The global seaborne market for oil products has long involved significant arbitrage trading. That’s to say, purchasing a cargo in one location and time, and selling it later at a higher price some place else.

Those arbitrages emerge because of the inherent nature of fuel markets: stockpiles become imbalanced if, say, a refinery halts and replenishments are needed. Extra cargoes move, and prices adjust until normality returns.

Europe’s imports ban will have a big impact on arbitrage trading. A finite pool of fuel buyers will be asked to purchase products they wouldn’t normally have taken in the past. What happens if their demand slumps and there just isn’t enough buying interest from elsewhere?

Might there be times when individual Russian prices go haywire because there simply aren’t enough buyers? Where would that leave the nation’s refineries?

7. Easy Fix

The crude price cap was set at a sufficiently high level to keep oil flowing.

Doing the same with fuels would allow non-European buyers to buy freely and allay concerns about access to shipping and services.

It would mean that all the tankers that can theoretically transport Russian fuels are able to do so in practice.

Share This:

More News Articles

Source link

#Cap #Russian #Fuel #Prices #Harder #Energy #News #Canadian #Oil #Gas #Industry #EnergyNowca